Beef Market Advisor

Saturday, May 27, 2006

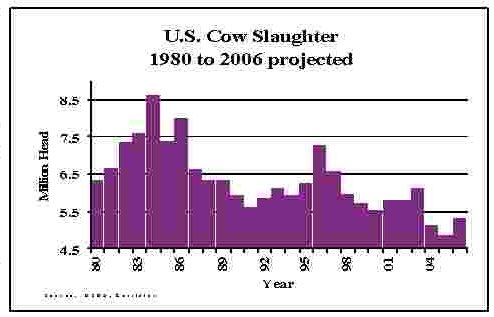

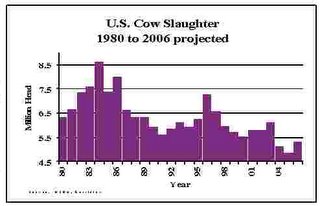

US COW SLAUGHTER UP 3%

US cow slaughter to May 6 is up 3.2% compared to 2005. The dry fall and winter in many of the southern states has lead to a recent increase in US cow slaughter.

March and April's levels were up 13% and 17% respectively. For the year. the current forecast is looking at a 9% increase over 2005 which would put 2006's total near 5.3 million head, still one of the smallest cow kills in history. The 2005 cow kill at 4.86 million was the smallest in recent times.

The drought conditions through the remainder of 2006 will play a key role in how many more beef cows come to town as culls. Cull prices have been about $5.00-7.00/cwt lower than last year and are expected to stay that way. Utility cow prices are between $50.00-52.00/cwt currently compared to $60.00 at this time last year.

-AD at CanFax, Canada.

posted by Dr. Harlan Hughes 1:46 PM [edit]

The Fed Cattle Summer Market Doldrums Started Early

By Derrell S. Peel, OSU Extension Livestock Marketing Specialist

Fed cattle markets have been disappointing in many ways in the first half of the year and that has many folks wondering what lies ahead for the rest of 2006. Fed cattle prices began the year strong off of the late 2005 rally but moved counterseasonally lower in the first quarter of the year. More recently, fed prices have stabilized somewhat but at lower levels than anticipated for this time of year. Summer is usually the seasonally low price time of the year for fed cattle and the question now is “How low will fed prices drop for the summer lows?” More fundamentally, why have fed cattle markets struggled so severely so far this year? Fed prices are struggling because of a complex set of supply and demand issues.

Supply issues have changed, more as a matter of timing than of a fundamentally larger supply potential. On January 1, 2006, feedlot inventories were already 3 percent above year earlier levels as aggressive feedlot demand and dry winter conditions combined to increase feedlot placements. Severe drought conditions in the southern winter grazing regions pushed many additional cattle to market ahead of schedule in January, February and March. These early placements, combined with a steady flow of Canadian feeder cattle pushed feedlot inventories to a record May 1 level that was 9 percent above the 2005 level.

The fed market psychology seems crushed under the idea that huge cattle inventories will weigh down the market for the rest of the year. It is important to remember that we don’t have anything near 9 percent more total feeder cattle available to push up feedlot production. On January 1 the estimated feeder supply in the U.S. was up less than 2 percent over the previous year. Allowing for a full year of Canadian feeder cattle imports in 2006, the potential annual feedlot production potential is perhaps a 3 to 4 percent increase over last year.

Feedlot placements were lower in April and will be lower still in May. Feedlot inventories will stay above year ago levels but will pull back significantly in the next couple of months. Exactly how far inventories will pull back will depend on forage conditions this summer as it affects the aggressiveness of heifer retention and on the rate of feedlot marketings. Total U.S. beef production is expected to increase about 5 percent, mostly as a result of more Canadian cattle being slaughtered in the U.S. Net U.S. beef supply is projected to increase less than 2 percent as increased imports of Canadian cattle are offset by reduced imports of boxed beef from Canada.

The other side of the supply increase has been extremely heavy carcass weights through the first half of the year. Cattle performance was good through the winter and feedlots have not had much incentive market cattle aggressively until recently. Through most of the first half of the year, heavy carcass weights added the equivalent of 15 to 20 thousand head per week to slaughter totals. Although carcass weights will likely remain above year ago levels, weights have moderated and there is significantly less incentive now compared to the last several months to increase fed cattle weights with higher feed costs and summer discounts on Live Cattle futures.

In the first quarter of 2006, demand limitations were a significant constraint to fed cattle prices. Boxed beef prices were limited by short run demand factors including increased competing meat supplies and higher energy prices. Tight meat packing margins resulted in intense pressure to limit fed cattle prices during this period. Moving into the second quarter, the supply pressures shifted the advantage to packers and fed cattle prices continued to weaken despite more stable boxed beef prices. At the current time, packing margins are much improved thereby reducing pressure on fed cattle prices while many feedlots continue to experience losses. Fed cattle prices are likely to remain in the $70s with an average summer low of roughly $75/cwt. expected. Feedlots are likely to continue to experience poor profitability through the third quarter of 2006.

There is reasonable hope for an improved fed cattle market situation in the last part of the year. Much of the current bulge of feedlot cattle will work their through feedlots in the third quarter of the year and supply conditions are expected to improve late in the year. Likewise, some of the competing meats issues will also improve in the second half of the year. Some of the demand uncertainties will remain, especially energy price impacts and potential impacts of Avian Flu in global meat markets. If these uncertainties do not actually manifest themselves as significant issues, it is likely that fed cattle prices are expected to recover back above the $80 level and could end the year in the mid $80s.

Oklahoma State University, in compliance with Title VI and VII of the Civil Rights Act of 1964, Executive Order 11246 as amended, Title IX of the Education Amendments of 1972, Americans with Disabilities Act of 1990, and other federal laws and regulations, does not discriminate on the basis of race, color, national origin, sex, age, religion, disability, or status as a veteran in any of its policies, practices or procedures. This includes but is not limited to admissions, employment, financial aid, and educational services.

posted by Dr. Harlan Hughes 10:19 AM [edit]

One calving season versus two calving seasons

By Glenn Selk, OSU Extension Cattle Reproduction Specialist

Deciding on the use of one calving season or two calving seasons is a big first decision when producers are choosing calving seasons. Many fall calving seasons have arisen from elongated spring seasons. Two calving seasons fits best for herds with more than 80 cows. To take full advantage of the economies of scale, a ranch needs to produce at least 10 to 20 steer calves in the same season to realize the price advantage associated with increased lot size. Therefore having forty cows in each season as a minimum seems to make some sense.

Using two seasons instead of just one can reduce bull costs a great deal. Properly developed and cared-for bulls can be used in both the fall and the spring, therefore reducing the bull battery by half. Another small advantage to having two calving seasons is the capability of taking fall-born heifers and holding them another few months to go in to the spring season and visa versa. Because of this replacement heifers are always 2 1/2 years at first calving instead of 2 years old. These heifers should be more likely to breed early in the breeding season and have slightly less calving difficulty. Research has shown that these differences are very small, therefore the cost of the other six months feed must be minimal to make this a paying proposition. Many producers like the dual calving seasons because of the spread of the marketing risk. Having half of the calf crop sold at two different times allows for some smoothing of the cattle cycle roller coaster ride.

There are however a couple of disadvantages that must be considered. The producer now has twice as many nights to get up and check cows and heifers at calving time. In addition, if heifers are not bred until about 20 or 21 months of age, then they will be more than 24 months of age when they are preg checked. Open heifers that need to be culled at more than 24 months of age will definitely be penalized at the market place compared to younger cull heifers that are sold at much higher prices per pound.

From the Oklahoma Cooperative Extension Service

posted by Dr. Harlan Hughes 10:17 AM [edit]