Beef Market Advisor

Tuesday, March 21, 2006

Market Comments

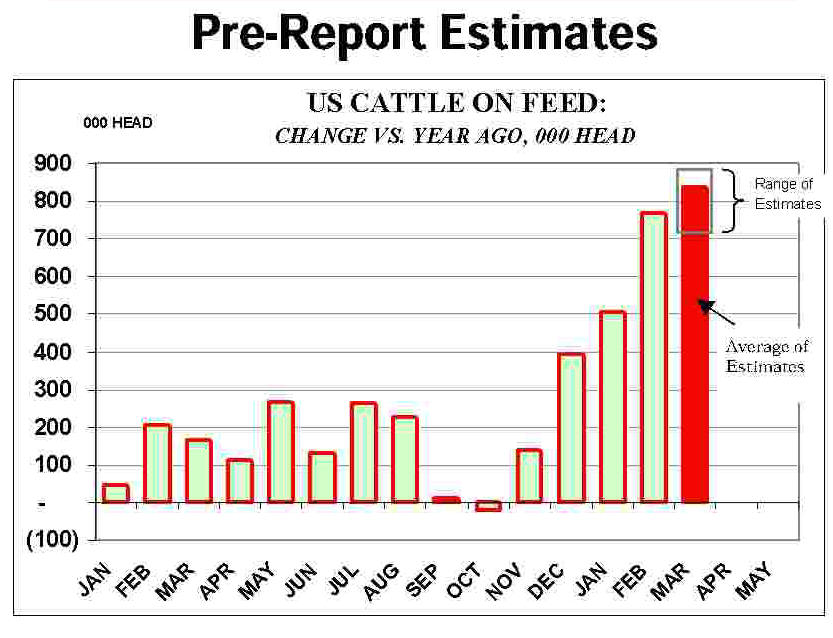

As the Chart shows, it is widely expected that the March 1 feedlot

survey will show a further increase in the number of cattle

currently on feed. Using the average of pre-report estimates, which

indicates a 7.5% increase in feedlot inventories, we come up with a

March 1 inventory of 11.991 million head, the largest March 1

inventory number and the second highest feedlot inventory EVER.

This inventory level would represent an 837,000 head increase vs.

year ago levels. These are all cattle that will have to be

processed by the end of this spring or early summer, a daunting

task given the current rate of marketings and the ongoing tug of

war between packers and feedlot operators.

Keep in mind that estimated breakevens for feedlots are currently

around $83-85 and efforts to pressure cattle prices lower means

feedlots will be forced to loose some real money.

The increase in feedlot supplies becomes even more significant when

considering the fact that the weight of cattle currently coming to

market is significantly higher than a year ago. Last week, USDA

reported cattle weights at 783 pounds, 27 pounds heavier than a

year ago. This increase in carcass weights is the equivalent of

27,000 more cattle com-ing to market last week.

It is hard to know what the actual weight of cattle currently on

feed is compared to a year ago, the only way we can find that out

is to wait until they are processed. However, the warm winter makes

it a safe bet to assume that feedlot weights are up and this means

that the supply of beef (rather than head of cattle) is actually

even more daunting than the attached chart shows.

Prices will continue to play an important role in the marketplace

in cleaning up the additional supply currently available. The

nearby live cattle contract (April) closed tonight at $83.475, more

than $9 per cwt (-10%) lower than where the 2005 April Live Cattle

contract settled on its last trading day.

The question is: Has the futures market already discounted the

large feedlot supply or will it take more price declines to find a

home for the product? This question will be resolved at the CME

cattle pit in the weeks ahead.

Source: CME Daily Livestock Newsletter 21 Mar 2006.

posted by Dr. Harlan Hughes 3:09 PM [edit]

Cyclically High-Priced Replacements & Cow Leasing

Realizing there are no one-size fits all answers to these questions, given the resources and goals of individual producers, in general terms:

Ø What are strategies that should be considered for managing the added equity risk of cyclically high-priced replacements (retained or purchased)?

[Harlan Hughes] answer: I think expanding cow numbers in a herd now is almost a sure recipe for loss equity by the end of the decade. I am convinced that expanding a herd now will definitely increase the average unit cost of producing a hundredweight of calf for the herd over the next several years. This all leads to reduced profits from the expansion.

Ø Is now the time in the cycle to consider expanding, holding steady or reducing numbers, i.e. how many calves does a replacement need to sell into the up-market to make it work?[Harlan Hughes] answer: it is the time to consider selling breeding livestock. I encourage producers to sell every calf born when prices are at their peak and to build a financial reserve for the tough time a' coming.

Ø Which price data sets do you find most useful in estimating the net present value of replacements?

[Harlan Hughes] Answer: I publish a set of long-run planning prices based off of FAPRI's Long-Run price simulations. North Dakota also publishes some long-run planning prices that ranchers could use.

Ø More specifically, do cow-leasing or other share arrangements provide an opportunity to manage the risk of the higher priced replacements at this stage?

[Harlan Hughes] answer: It could provided the lease arrangement is equitable. But, these leases can turn negative for the working rancher as prices trend downward as projected for the rest of this decade.

Ø If a producer has never leased or shared cost/income with someone else, what are key questions they should answer for themselves in determining if this is an approach they should consider?

[Harlan Hughes] answer: The lease has to equitable, that is, fair for both the cow owner and the working rancher. Cull cow income goes to the cow owner. Heifer development needs to be outside of the lease arrangement. The lease needs to be in writing. And one final point. Leasing cows does not increase the profit for those cows and the profit from leased cows is always shared. I sometimes think people believe that leased cows generate more profit. No, and it is shared by two parties.

posted by Dr. Harlan Hughes 1:09 PM [edit]

Sunday, March 19, 2006

This Week That Just Passed Was A Mixed Bag For The Cattle Industry

Nearby live cattle also bounced back from the lows reached in mid week and were just 25 points shy of last Friday's close. Feeder cattle futures, on the other hand, rallied hard from the lows registered early in the week and closed the week 140 points higher than a week ago.

Despite the fact that this week turned out to be a very forgettable one, it also did little to alleviate much of the bearish mood currently prevailing in the livestock futures complex. Judging by the supply data on the attached table, there simply is too much meat protein coming to market at a time when export and domestic demand is underwhelming, at best. Consider the following:

Beef production this week was up 9.3% from a year ago.

Pork production this week was up 4.5% from a year ago.

Chicken production this week was up 4.9% from a year ago.

Turkey production this week was up 5.4% from a year ago.

The overall increase in production represented a 115 million pound additional supply created in a single week. And this was not just a one time thing but rather the latest data point in a trend of higher meat supplies. The four week moving average is currently almost 5% higher than a year ago and the 12-month moving average is 3% greater than the previous year.

Such increases in supply are taking place at a time when beef export markets are stunted and 60% smaller than they were prior to the BSE outbreak and chicken export markets are growing slowly due to bird flu in much of the world.

BUT... we have seen a similar situation not very long ago, only in reverse. Not long ago, beef, pork and poultry executives seemed to do no wrong, prices were strong and, in the case of pork, kept getting stronger.

If the cure to high prices is high prices, the same is true for low prices also, eventually but not today.

Source: CME Daily Livestock Report 17 March 2006.

posted by Dr. Harlan Hughes 10:44 AM [edit]