Trends ... U.S. COW AND HEIFER SLAUGHTER BELOW A YEAR AGO

Federally Inspected (FI) cow and heifer slaughter levels have been well below a year ago in 2005. The smaller number of cows and heifers in the slaughter mix confirms that U.S. producers have fully entered the cowherd-rebuilding phase of the cattle cycle. The tighter supply of slaughter cows has supported rather strong slaughter cow prices this year.

From January through October, FI cow slaughter was down 6.5 percent from the respective period a year ago and nearly 17 percent lower than the prior five-year average (1999-2003). FI beef cow slaughter at 2.1 million head was down 7.4 percent, while dairy cow slaughter was 5 percent smaller than the respective ten-month period in 2004. Weekly slaughter data for November, suggests cow slaughter was seasonally larger with a year-to-year increase of 2 percent, but still well below the prior five-year average.

FI heifer slaughter in the U.S. totaled 8.2 million from January through October, down 528 thousand head (6 percent) from 2004's. Thus far this year, monthly heifer slaughter was at its lowest in February at 751 thousand head, which was the lowest monthly number since May 1993 (also 751 thousand head). November weekly slaughter data showed heifer slaughter up around one percent from 2004's, but 14 percent lower than the prior five-year average level. Of the total steer and heifer slaughter mix, heifers have accounted for 37 percent from January through November this year.

The annual January 1 U.S. cattle inventory numbers (to be released by USDA-NASS on January 27, 2006) will show an increased cowherd and estimates for tight feeder cattle supplies outside feedlots. In fact, nationwide feeder cattle supplies outside feedlots could be smaller than a year earlier as of January 1, 2006, if U.S. feedlot placements remain large in December.

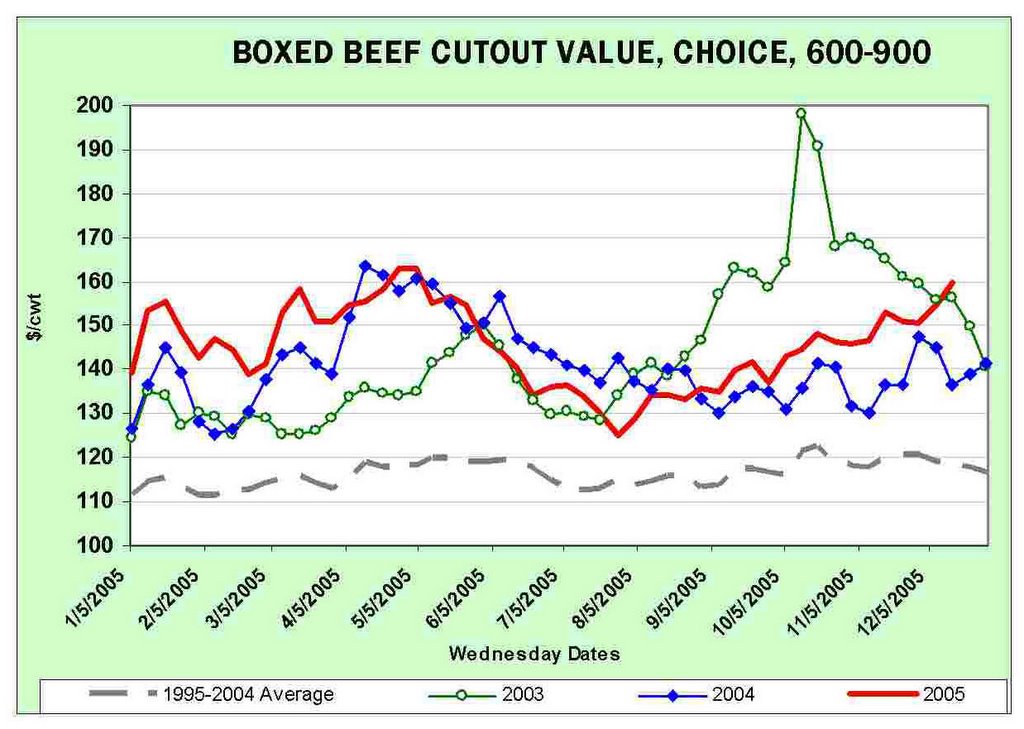

Source: Livestock Monitor, WLMIC Dec 16, 2005

posted by Dr. Harlan Hughes 3:51 PM